Costs, Running & Reality

The Real Barrier to Campervan Ownership Isn't the Price. It's the Finance.

Written by

Oliver

Oliver is the founder of Campervan.win and writes about campervans, travel, and the life-changing freedom that comes with getting out on the road.

The short answer

The real barrier to campervan ownership is not just the rising price but the lack of finance incentives, and naming that clearly is the first step to fixing it. New panel-van prices rose 15 to 23 percent between 2021 and 2023, with a further 3 to 5 percent signalled for 2026, so anything with a proper bathroom and kitchen now starts above £60,000. Yet unlike cars, EVs or phones, campervans have almost no 0 percent deals or deposit contributions: a £65,000 van on five-year HP is £700-plus a month, competing with rent or a mortgage. That quietly locks out younger buyers who would otherwise love the lifestyle, a gap that targeted 0 percent deals could close. Campervans have never been more desirable; they just need to be more reachable. Here is what is really holding people back, and what could change it.

Campervans are expensive. That is not news to anyone who has browsed a dealer's forecourt or scrolled through AutoTrader in the last couple of years. A new panel van conversion that might have cost £45,000 in 2019 now starts at £60,000 or more. The prices have gone up, and they are not coming back down.

But here is the thing. The rising prices, while frustrating, are understandable. The real problem is something the industry barely talks about: there are almost no meaningful finance incentives to help people actually afford these vehicles. And that is locking out an entire generation of potential buyers.

Why Prices Have Gone Up

The campervan market has been through a lot since 2020. During the pandemic, demand went through the roof as people looked for ways to holiday safely. At the same time, supply chains collapsed. Semiconductor shortages hit base vehicle production. Raw material costs for steel, aluminium and timber all spiked. Fiat, the chassis supplier behind the majority of European campervans, raised their prices repeatedly.

Between 2021 and 2023, average new motorhome and campervan prices increased by anywhere from 15% to 23% depending on the segment. Manufacturers have signalled further price increases of 3% to 5% for 2026 models. Production volumes still have not returned to pre-pandemic levels. Several manufacturers have actually reduced their model ranges rather than scaling up, focusing on fewer models that sell reliably rather than trying to cover every niche.

None of this is unreasonable. Materials cost more. Labour costs more. The Fiat Ducato chassis that underpins most campervans costs more. Manufacturers need to charge prices that reflect their actual costs, and dealers need margins that keep their businesses viable. Nobody benefits from artificially cheap campervans built with cut corners.

The market is adjusting. Used prices have softened slightly as new-old stock from 2023 and 2024 gets discounted on forecourts. There are deals to be found if you are flexible on spec and willing to buy a model year that has been sitting around. But the days of new campervans under £50,000 are largely behind us, at least for anything with a proper bathroom and kitchen.

That is the reality. And most people accept it.

The Finance Gap

What people struggle with is not the sticker price itself but the complete lack of help getting there.

Think about the car market for a moment. Walk into any car dealership in the UK and you will be offered 0% finance, deposit contribution schemes, trade-in bonuses, balloon payment structures, low-rate PCP deals, manufacturer-subsidised APR offers. The car industry spends billions making it as easy as possible for people to afford their products. These incentives are not charity. They are carefully calculated tools that drive volume and build brand loyalty.

Now try buying a campervan.

The finance options are typically straightforward hire purchase agreements at whatever the going interest rate happens to be. There are no 0% deals. No manufacturer-subsidised rates. No deposit match schemes. No creative financing structures designed to bring monthly payments down to accessible levels. You either have the cash, qualify for a standard loan at market rates, or you do not buy one.

For a £65,000 campervan on a typical 5-year HP agreement at current interest rates, you are looking at monthly payments of £700 or more. That is a serious commitment. And unlike a car, where you might finance £25,000 and the monthly payment sits comfortably alongside a mortgage, a campervan finance agreement is competing with rent or mortgage payments for available income.

A Generation Priced Out

This is where it gets frustrating. The campervan lifestyle has never been more popular with 20 to 30-year-olds. Social media is full of young couples converting vans, documenting their travels, building a life around freedom and adventure. The vanlife movement is not a marketing invention. It reflects a genuine shift in what younger people value: experiences over possessions, flexibility over fixed addresses, travel over traditional milestones.

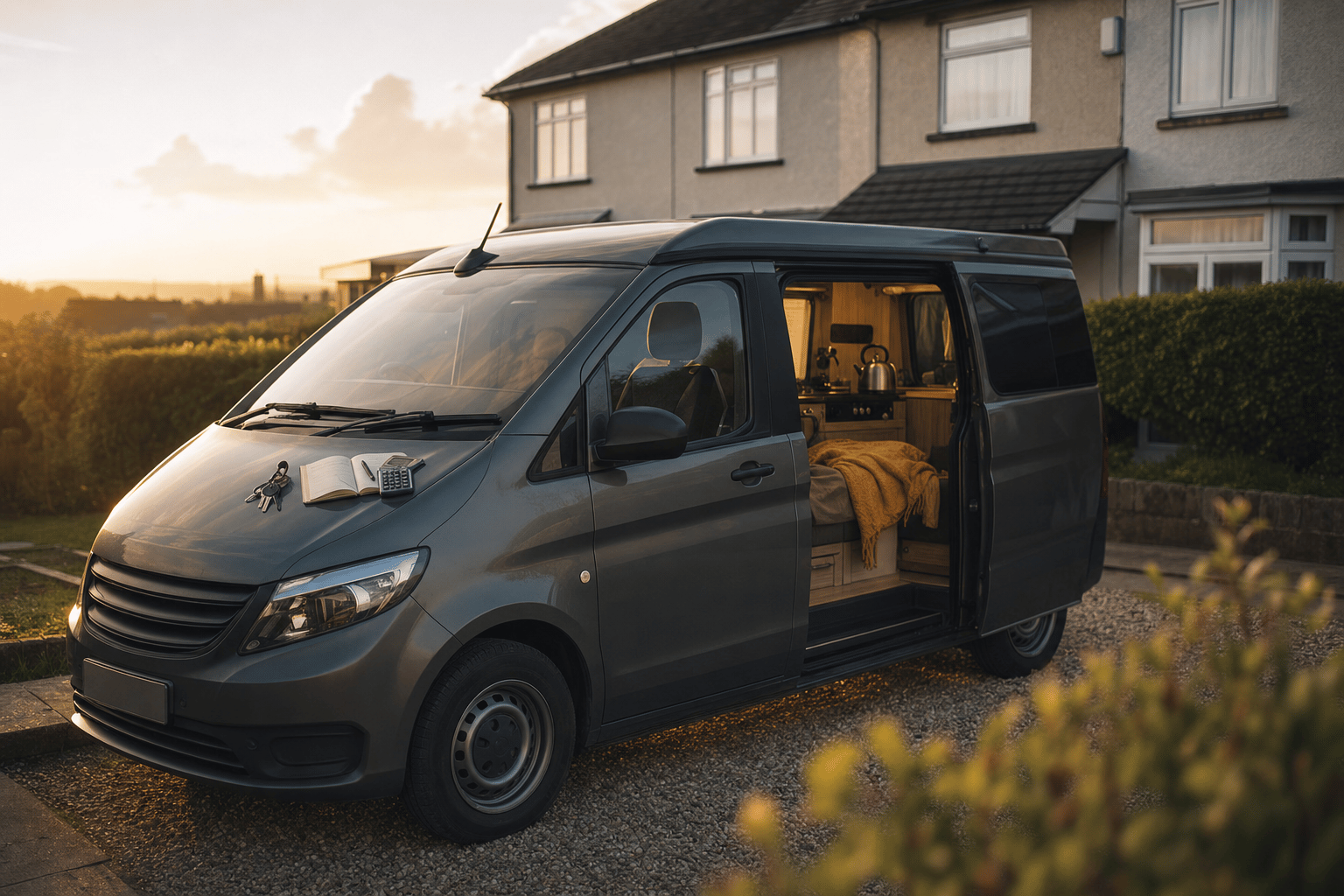

A campervan like the Sunlight Vanlife at around £62,000 would be a dream for a lot of these people. It is compact enough to daily drive, equipped enough to live in for extended periods, and affordable enough to be within touching distance of a reality. But without decent finance options, "within touching distance" stays exactly that. Close but out of reach.

A 25-year-old couple, both working, earning a combined £50,000 to £60,000 a year, would struggle to get approved for a £62,000 HP agreement at standard rates, let alone comfortably afford the repayments. These are exactly the people the Sunlight Vanlife was designed for. Sunlight's own marketing targets young, adventurous travellers. But the financial infrastructure to actually sell to those people barely exists.

Compare that to the electric car market, where manufacturers routinely offer 0% or near-0% finance over 3-4 years specifically to bring younger buyers into the fold. Or the smartphone market, where 0% interest spread payments are standard. These industries understand that if you want younger customers, you have to meet them where they are financially.

What Needs to Change

The campervan industry should be offering interest-free finance options. Not on every model. Not forever. But targeted 0% deals on entry-level and mid-range campervans that bring monthly payments to a level where younger buyers can realistically commit.

A 0% deal on a £62,000 Sunlight Vanlife over 4 years would work out at roughly £1,290 per month. Still significant, but manageable for a couple splitting the cost who see it as their primary vehicle and their accommodation rolled into one. Over 5 years at 0%, that drops to around £1,033 per month. For people who would otherwise be spending £800 on rent plus £300 on car finance, the maths suddenly starts to make sense.

Manufacturers could subsidise these rates and absorb the interest cost as a customer acquisition tool, exactly the way car manufacturers do. Dealers could partner with specialist lenders to create campervan-specific products with longer terms and lower monthly payments. The industry bodies could lobby for campervans to qualify for green travel incentives, given that a couple living and travelling in one vehicle is considerably more carbon-efficient than maintaining a house and a car separately.

None of this is radical. It is just standard practice in almost every other high-value consumer market applied to campervans.

The Opportunity

The demand is there. Auto Trader reported a 59% increase in advert views for motorhomes, caravans and campervans over the last five years. One in five Brits surveyed said they were planning a motorhome or caravan holiday in the next 12 months. That is 20% of the population expressing active interest. The market is not shrinking. It is growing. But it is growing among people who increasingly cannot afford to buy in without help.

The manufacturers who work this out first will have a significant advantage. The first brand to offer genuine 0% finance on a well-specced campervan under £65,000 will dominate the conversation among younger buyers. They will build brand loyalty that lasts decades, because the couple who buys their first campervan at 28 is likely still buying campervans at 58.

Prices going up is a fact of life. The cost of materials, engineering, and compliance is only heading one direction. But the industry has a responsibility to make ownership achievable, not just aspirational. And right now, the gap between aspiration and reality is a finance application with no incentives and an interest rate that turns a dream into a burden.

Campervans have never been more desirable. The industry just needs to make them more accessible.

At Campervan.Win, we believe everyone should have a shot at campervan ownership. That's why we run monthly competitions where you can win campervans, motorhomes and outdoor gear for as little as £7.50 per entry. No finance applications required. Visit campervan.win to see what you could win this month.

Common questions

Why are campervans so expensive now?

A mix of forces since 2020: pandemic demand spiked while supply chains collapsed, semiconductor shortages hit base-vehicle production, and steel, aluminium and timber costs jumped, with Fiat (the chassis supplier behind most European campers) raising prices repeatedly. The result is that average new prices rose 15 to 23 percent between 2021 and 2023, with another 3 to 5 percent signalled for 2026.

What is the real barrier to campervan ownership?

Not just the price, but the finance. The industry barely offers meaningful finance incentives, so unlike cars, EVs or smartphones, there are almost no 0 percent deals, deposit contributions or subsidised rates on campervans. That turns a high price into unaffordable monthly payments and locks out an entire generation of would-be buyers.

How much are monthly payments on a campervan?

Steep. For a 65,000-pound campervan on a typical five-year HP agreement at current interest rates, you are looking at 700 pounds or more a month. And unlike a car loan that sits alongside a mortgage, a campervan payment competes directly with rent or a mortgage for available income, which is why it is so hard for many people to afford.

Why can't younger buyers afford campervans?

The lifestyle has never been more popular with 20 to 30-year-olds, but the finance does not work. A 25-year-old couple earning a combined 50,000 to 60,000 pounds would struggle to be approved for a 62,000-pound HP agreement at standard rates, let alone afford the repayments, especially with no 0 percent deals like those routinely offered on electric cars to bring younger buyers in.

Would 0 percent finance make campervans more affordable?

Significantly. A 0 percent deal on a 62,000-pound campervan over four years works out at roughly 1,290 pounds a month, dropping to around 1,033 over five years, against 700-plus at standard HP rates. For someone already spending 800 pounds on rent and 300 on car finance, targeted 0 percent deals on entry and mid-range campervans are where the maths starts to make sense.

Is demand for campervans still strong?

Yes, despite the prices. Auto Trader reported a 59 percent increase in advert views for motorhomes, caravans and campervans over the last five years, and the lifestyle is more desirable than ever. The issue is not desire but accessibility: the industry needs to make ownership achievable, not just aspirational, and finance is the missing piece.

The reachable bit

The camper you fall for is rarely the one you can afford. That gap is the whole reason Campervan.win exists. Right now we’re giving away the Sunlight Vanlife, worth around £65,000, and closing that gap is the point: capped entries so the odds stay honest, £10 a ticket, a maximum of five per person, £500 to a UK charity from every full draw, the winner picked by a public randomness beacon anyone can re-check, and one person driving away in the van itself.

Enjoyed this post?

Get more honest campervan guides like this one in your inbox.

You’re in!

Check your inbox. We’ve just sent you a welcome email.

About the author

Oliver

Oliver is the founder of Campervan.win and writes about campervans, travel, and the life-changing freedom that comes with getting out on the road.

Keep Reading

Related Reading

Thoughtful articles that build on what you’ve just read.

Costs, Running & Reality

26 min read

Motorhoming on a budget: the real ways to cut costs without cutting trips

An honest, detailed guide to spending less on motorhome life without staying home, from cheaper park-ups and smarter fuel use to insurance, maintenance and clever kit choices.

Costs, Running & Reality

15 min read

Should you buy a campervan, or just hire one? The honest maths

Should you buy a campervan or just hire one when you need it? The honest answer hinges on a single number most people get wrong: how many weeks a year you'll really use it. Here's the real maths, the hidden costs of owning, and the decision laid out plainly.

Costs, Running & Reality

10 min read

A Campervan Gets You to the Coast. Surfers Against Sewage Is Fighting to Keep It Worth the Drive.

A campervan gets you to the coast. It can't make the water clean once you're there. Here's why £500 from this draw goes to Surfers Against Sewage.

Costs, Running & Reality

15 min read

Amandaland’s VW WestFalia Campervan and the Unsexy Truth About Campervan Toilets

Amanda hires a VW Westfalia in Amandaland and discovers the hard way that charm is not the same as convenience. A practical guide to campervan and motorhome toilet options, with honest pros, cons, and recommendations.